Daily Exasperation #1

The Uber PR machine sucks but they did turn a profit...finally. Does it matter?

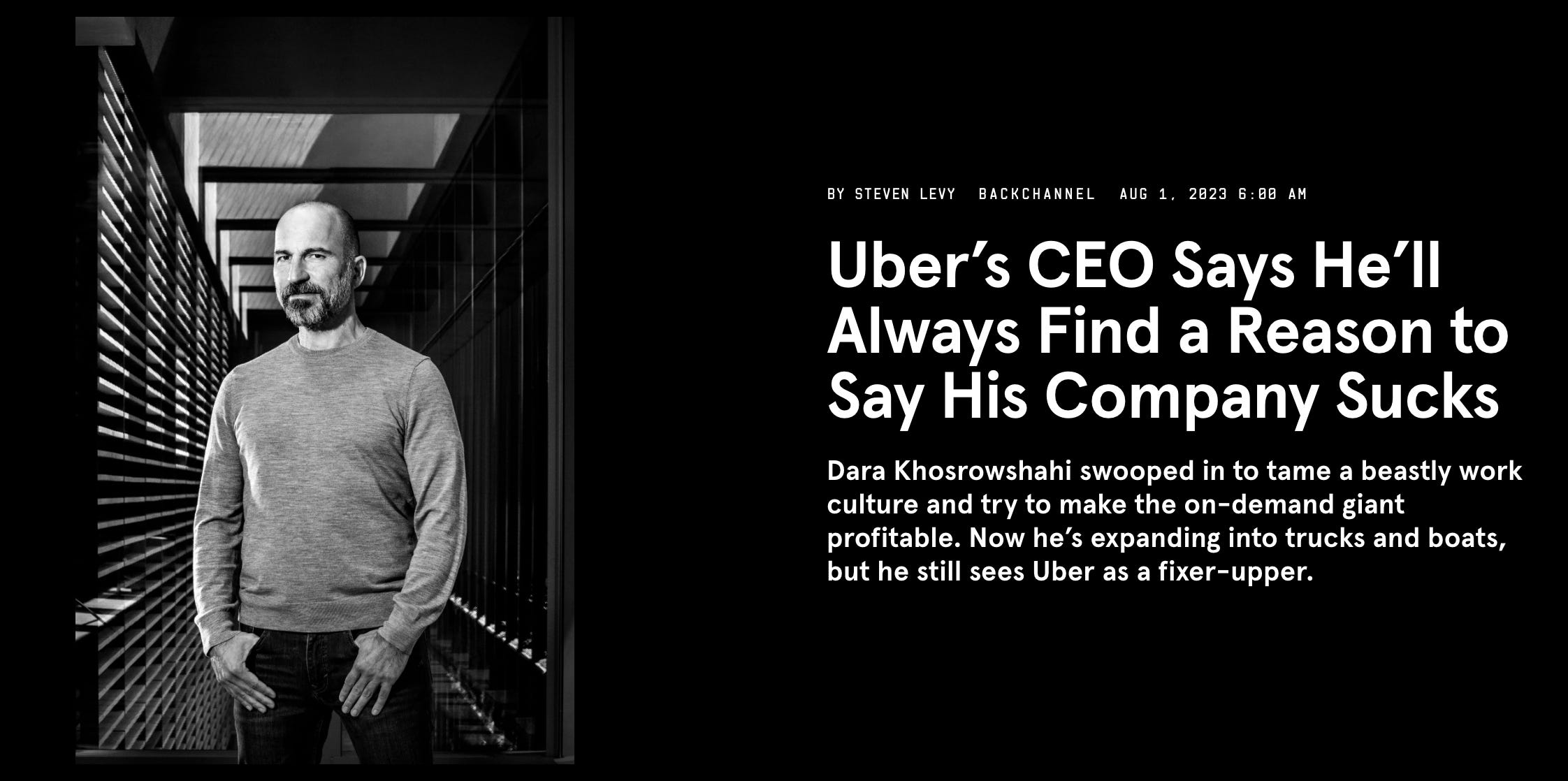

“FIFTY-ONE DOLLARS AND 69 cents. That was the charge, including tip, for the 2.95-mile trip I took last May from my downtown New York City apartment to the West Side facility where Uber was holding its annual product event, called Go-Get. The ride-hailing company’s charges have been higher in recent years, and fluctuate in any case, but that was nuts.”

— “Uber’s CEO Says He’ll Always Find a Reason to Say His Company Sucks,” Steven Levy, Wired, 8/1/23 (accessed 8/2/23).

My problem with this is that the Subway would have cost Mr. Levy $2.75, but that doesn’t make for a good story. Yes, As Mr. Khosrowshahi points out there are use cases for Uber and use cases for the Subway, and yes there’s an option to search for transit inside Uber’s app, but, and be honest, once you’ve opened up Uber, it’s highly unlikely you’re searching for the best Subwa…